The banking system in South Africa is highly developed, and the country also has excellent internet access. With widespread access to smartphones and a growing preference for conducting business online, the digital banking industry is poised for explosive growth.

Mobile Banking in South Africa: an Overview

As in other countries, many people in South Africa prefer using cash. However, more and more people in South Africa are trying out novel approaches to personal finance. Specifically, via means of a mobile application.

The first thing to keep in mind when thinking about mobile banking in South Africa is the distinction between brick-and-mortar retail banks and online-only banks (sometimes known as challenger banks or digital banks). Both provide mobile banking, but there are key distinctions to be aware of.

Online Banking Convenience: A Comparison Shop

There is less of a need for customers to physically visit a bank office thanks to the rise of mobile banking. Since they don’t have to spend money on brick-and-mortar facilities like ATMs or branches, fully digital banks may sometimes undercut their more conventional competitors on pricing.

Despite their increasing prevalence, digital banks aren’t without their drawbacks when compared to more conventional retail banks, particularly for foreigners relocating to South Africa. That’s why you must do your homework before committing to a bank in South Africa. This helpful guide compares and contrasts the mobile banking features of both online and brick-and-mortar financial institutions.

Banks in South Africa Now Provide Mobile Banking

ABSA, FirstRand (FNB), Nedbank, and Standard Bank are the Big Four retail banking titans in the rainbow nation. Capitec Bank, known for its competitive rates, is quickly becoming a household name. These well-established financial institutions all offer mobile banking services. The satisfaction of customers varies commonly from one financial institution or app to another. However, South Africa’s financial institutions are highly regarded around the world.

Find Out What You Need to Open a Bank Account in South Africa

While all banks make some sort of social impact, ‘green bank’ Nedbank stands out thanks to its affinity programmes. In this way, you may balance your support for environmental, athletic, and charitable organisations with your budget.

App-enabled South African Banks

Each of South Africa’s conventional banks, as was previously indicated, offers its dedicated mobile banking app. According to a 2021 customer satisfaction poll, they are ranked below from most to least popular:

- ABSA

- Capitec

- FNB

- Standard Bank

- Nedbank

The banking applications from Capitec and FNB have both been lauded for their innovative features. They are known for regularly updating and improving their software. Nedbank’s app is well-liked for its clarity and use but receives lower marks for originality. In the meantime, Standard Bank and ABSA have released mobile apps that customers have said are of lower quality than those of their competitors and even frequently crash. However, much like any other digital service, FNB, and Capitec mobile banking apps are susceptible to outages.

Functions of a Mobile Banking App

Competing mobile banking apps often offer a wide variety of features. However, often when you launch a mobile banking app in South Africa, you’ll be able to do the following:

- To test one’s equilibrium.

- Send and confirm money transactions across borders.

- Schedule regular payments.

- Adjust your card’s spending cap.

- Card cancellation/reordering.

- Create a corporate or personal bank account.

- Submit Credit and Loan Applications.

- Watch your credit rating closely.

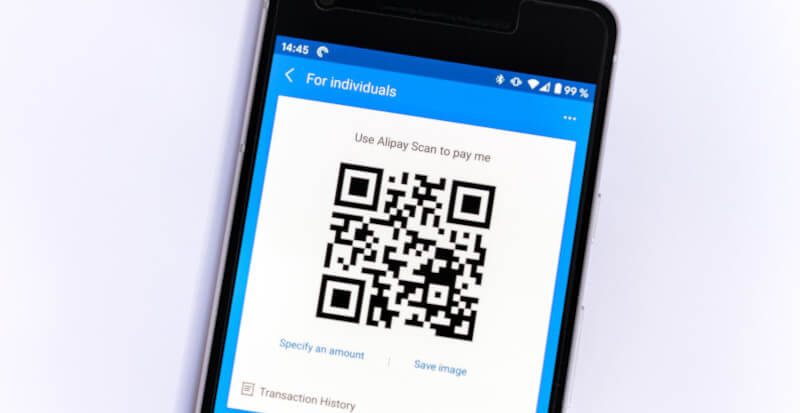

- Scanning QR codes for payment.

- Get some mobile data and airtime for your phone.

- You can now edit your beneficiary information online.

- Submit an Insurance Application.

- Move money around between accounts.

- Donate money or pay fines.

- Modify your information.

The Convenience of Banking App Payments

As was previously said, these apps allow for cross-border financial dealings. Remember that residents can send up to R1 million annually tax-free through the international money transfer system. Standard Bank also offers virtual cards that may be used to shop online without revealing any financial information.

South African Mobile Banking Basics

You’ll need a bank account in South Africa before you can use a retail bank’s mobile banking app. Depending on the institution, you may be asked to supply additional information throughout the enrollment process, such as a photo ID, proof of residency, and maybe biometric information. Read our how-to on creating a bank account in South Africa for further details on the registration procedure.

Do Your Research

Information on how to utilise the bank’s mobile banking apps is normally supplied after account opening. If not, you may always look it up online or contact a representative. You can access your account from your mobile device after installing the app and finishing the authorisation process. Keep in mind that identification using fingerprints and/or Face ID may be required for the authorisation procedure.

Costs Associated With Using a Mobile Banking App

South Africa’s online banking industry is notable for its upfront pricing policies. Since they don’t have the same need for infrastructure like ATMs and physical locations, they may provide substantially lower fees than conventional banks. They also provide fewer services, but that makes sense. Furthermore, most banks simply charge for transactions and not every month. Keep in mind, though, that both online and brick-and-mortar banks will tack on a fixed fee, anywhere from R2 per R100 withdrawn to roughly R6 or R7 per R1,000 withdrawn.

The excellent news is that both the applications and the transactions performed within them do not cost anything. It’s important to remember, too, that the going rate for a standard checking account in a brick-and-mortar bank in South Africa is between R89 and R120 a month. Withdrawal and payment fees may also apply, depending on the financial institution. The natives claim there is “nothing for mahala” (free/nothing).

Keep in mind that banking costs in South Africa may be higher than those in other countries in some circumstances. The answer to this question is largely conditional on the specific services and financial dealings you have in mind. Take your time and make sure you understand everything involved.

Compare Mobile Banking Service Plans and Fees

For additional information, please visit the respective online banking websites. You may get detailed descriptions of their pricing structures, allowing you to plan your splurging with confidence.

South Africans Use Mobile Payment Systems

In South Africa, mobile phone payments, outside of in-app purchases, have been available for some time. SMS payments, in which you send money by simply dealing an amount on your phone and following the prompts, have been around the longest. This method also works for purchasing data or airtime (phone credit). This form of mobile banking does not require a smartphone, making it more widely available. In the city, it’s easy to use a Near Field Communication payment method, such as a QR code. PayPal and digital currencies like Bitcoin are accepted by some South African businesses.

South Africa’s Digital Banking System

In South Africa, “challenger banks,” sometimes known as “digital banks,” are all the rage right now. Sadly, South Africa’s digital banks currently exclusively serve South African nationals and permanent residents. If you’re in South Africa on a visa for employment or another type of temporary visa, for instance, you won’t be able to use these online banks.

TymeBank, a South African financial institution, has created waves in recent years, attracting consumers with its innovative digital offerings in just two. With the success of digital banks like Europe’s N26, local digital users are following suit. TymeBank has less bureaucracy than conventional banks but none of their infrastructure. Keep in mind that this and other digital banks in South Africa will not open an account for non-permanent citizens of South Africa, unlike N26. However, new systems are in development, so things may alter shortly.

Most South African online banks, with the possible exception of SpotMoney, don’t allow customers to apply for loans or establish credit. SpotMoney, on the other hand, is not a traditional bank so much as a loan and coverage aggregator that works similarly to a digital wallet. You can make minor purchases with TymeBank and pay for them later without incurring any interest. A credit card is also available. However, these financial institutions normally do not provide mortgages or loans.

New and Upcoming South African Banks

As was previously noted, only Mzansi (South African) children or permanent residents are eligible for digital bank accounts at this time. If this describes you, the good news is that you now have more banking options than ever before. These trendy new digital banks have, without a doubt, shaken up the South African banking industry. Therefore, millions of people in South Africa are becoming members. Some examples of South African digital banks are:

- Bank of Africa

- MyWorld Bank

- Discovery Bank

- SpotMoney

- Tyme Bank

Creating a Bank Account Online

In South Africa, you can establish an account with a digital bank if you meet the requirements. While the steps required to open a mobile banking account may vary by institution, the first stop should always be the bank’s website. Following the on-screen prompts, you can then register for an account and start downloading the app.

Study the Topic of Online Banking Safety

Authentication of your identity and place of residence in South Africa is required within the app. Your fingerprints and a selfie taken by you will act as your biometric information. Keep in mind that you’ll also need a valid cell phone number in South Africa. Everything should be operational, and your bank card, if you requested one, should be on its way to you, in the next few business days.

Safeguarding South Africa’s Banks

South Africa is not immune to global trends in financial and cybercrime. As a result, financial institutions place a premium on cyber security. Many banking apps now need a password or PIN in addition to fingerprint or facial identification to log in and make a transaction. Alerts will be emailed to you, and one-time approval codes will be issued to you, respectively. In addition, you can modify your PIN whenever you choose within the programme itself. You should contact the bank via the app right once if you suspect fraud has occurred. Be sure to get insurance for identity theft to help prevent and support any fraudulent situation.

Avoid Doing Mobile Banking Over Public Wifi

Some South Africans are hesitant about utilising mobile banking despite the efforts made by both traditional and digital banks to ensure the safety of their customer’s financial data. Here are some precautions you may take to avoid becoming a victim of mobile banking fraud:

- Codes should be kept confidential at all times.

- Never give out your debit card information to anyone, online or in person.

- Make sure your financial gadget is safe.

- Keep a close eye on your checking account.

- Don’t use a public Wi-Fi connection to access your bank account.

- Convert your transactions into alerts.

- Immediately notify the bank of any problems and comply with any requests made by the bank.